By Special Correspondent

African banks need to take the lead in more effectively organising and deploying the continent’s capital for investments that will boost growth, top bank executives said.

“Capital is available but it’s not being channeled into the opportunities that exist in Africa,” Aigboje Aig-Imoukhuede, chairman of Access Holdings, which owns Nigeria’s largest bank, said at the African Financial Summit in Casablanca earlier this month.

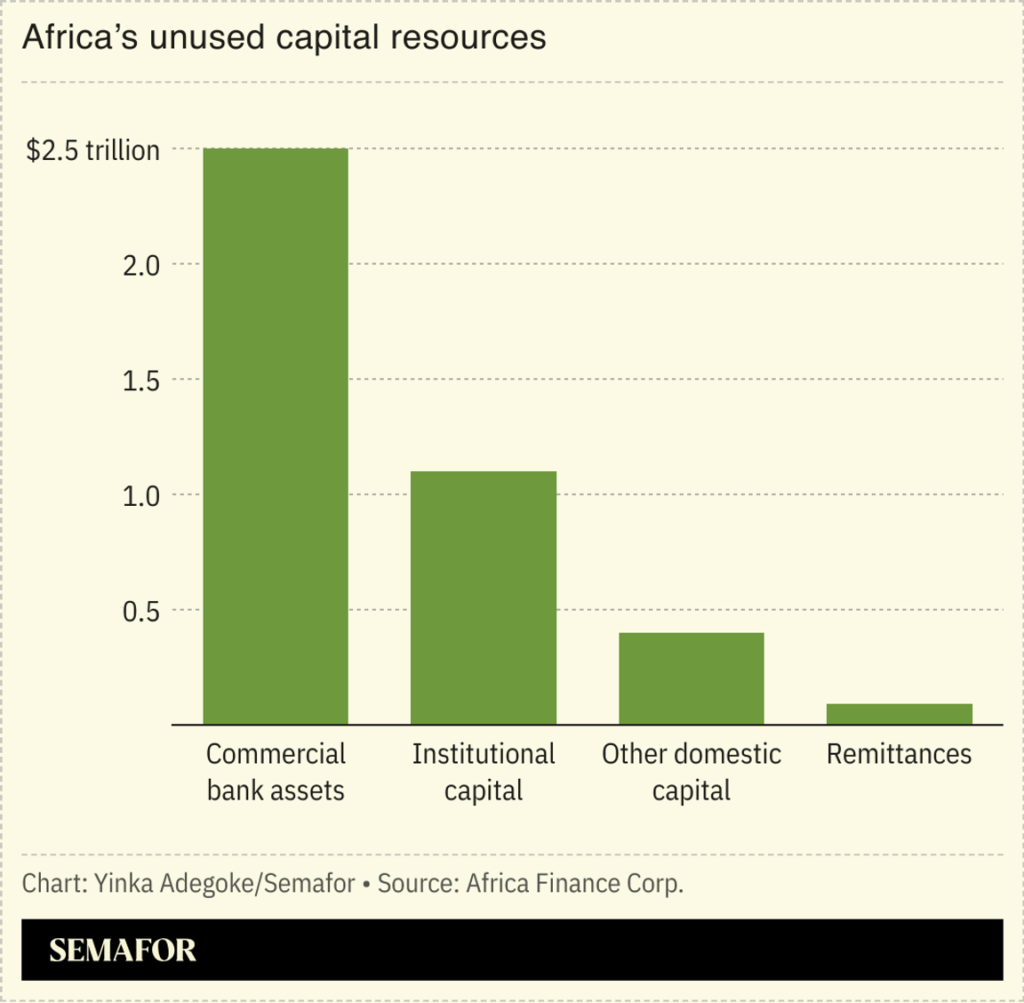

About US$4 trillion is estimated to be available across various sovereign and private money stores in Africa, according to the Africa Finance Corporation. It is a level of capital that can be absorbed by African economies to attend to many development needs, the challenge being one of efficient allocation, industry leaders said.

“We need more pension funds, sovereign funds and others to invest in the capital of banks, for us to lend to small and medium enterprises and the productive sector,” said Jeremy Awori, chief executive officer of the Ecobank group that operates in 34 sub-Saharan African countries, at the same event.

“We should not just be investing in sovereign paper,” he said, alluding to a perception that most African domestic financial assets flow towards short-term government securities.

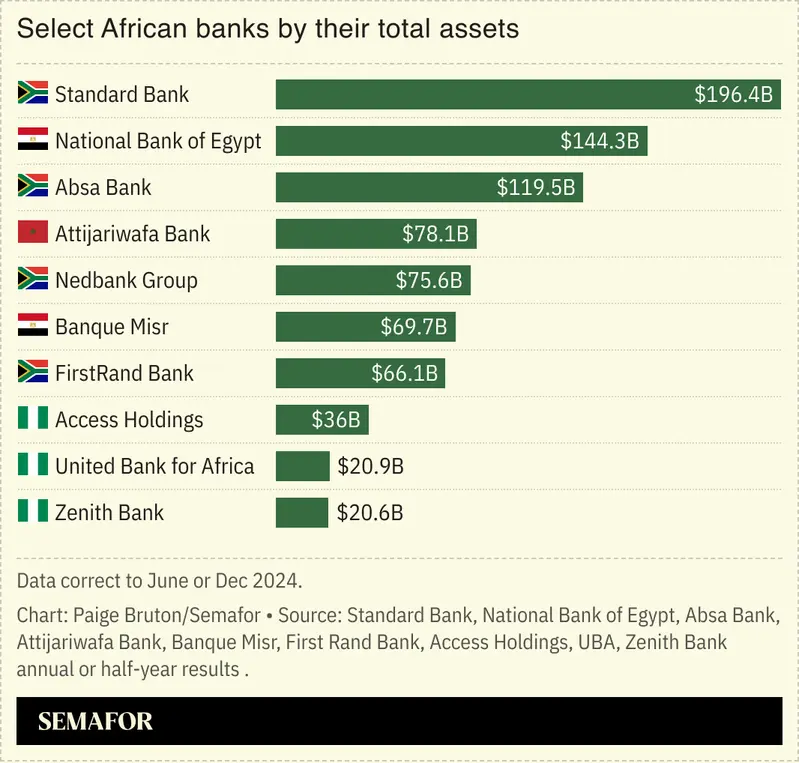

The top ranks of African banking are dominated by firms in northern Africa and South Africa whose assets range from tens to hundreds of billions dollars. South Africa’s Standard Bank is the largest with US$196 billion in assets.

Relatively smaller bank groups like Access Holdings have embarked on an expansion drive over the past few years to build a pan-African network able to provide cross-border capital deployment services.

It concluded a US$110 million deal this month to acquire the National Bank of Kenya from the Nairobi-based KCB Group. Access Holdings’s total assets rose by 26% to US$35.8 billion in the year to September, boosted by a near-50% increase in customer deposits.

The rise of fintech has driven up savings and payments volumes in Africa, but only two percent of about 700 million African bank accounts are applied towards investments, by Aig-Imoukhuede’s estimation.

“We need the right policy context to get hundreds of millions of Africans investing at scale, not just saving,” he said.

African fintech should diversify such that startups become “investment powerhouses,” partnering with traditional banks for the kind of scale that can produce transformative impact, he said.

Despite these ambitions, there is still an understanding that African banks operate in an economic environment with certain limitations that do not apply in developed markets or even other emerging markets.

While Asian banks, for example, operate in export-led economies that are parts of sophisticated regional trade networks, African banks are in economies whose health fluctuates to the tune of commodity prices and the landmark African free trade agreement has yet to fully take off, said Xavier Jopart, a financial services advisor at McKinsey.

Compared to the liquid financial markets in places such as Tokyo, Hong Kong, Jakarta and Singapore, capital market activity in Africa remains nascent and even shallow, Mr. Jopart said.

“It doesn’t help our banking sector that only 15% of trade on the continent is within Africa,” said Afreximbank executive vice president Haytham El Maayergi, partly due to road and port infrastructure designed by former colonial powers to ship goods to Europe.

Africa’s leading banking groups are targeting DR Congo, enticed by one of the continent’s fastest-growing economies and the promise of a lucrative mining sector, despite the ongoing conflict in the country’s east.

Top banks from Kenya, Nigeria, Tanzania, and South Africa are among the newly arrived or expanding institutions over the past 18 months as their leaders eye a market that still produces higher than average banking profits.

Local banks are starting to face more intense competition and, alongside earlier African entrants, are lobbying regulators and local politicians as tighter ownership caps rules are being considered.

SIDE BAR

Tanzania’s banking sector rides a wave of resilience and growth amid global headwinds

Tanzania’s financial sector extended its steady growth trajectory through 2024, buoyed by the economy’s resilience to global shocks, robust capital and liquidity buffers, and effective policy interventions by the Bank of Tanzania (BoT).

Performance across financial institutions continued to strengthen, as reflected in key balance sheet indicators – including total assets, deposits, capital adequacy, and liquidity positions – as well as improvements in core Financial Soundness Indicators (FSIs).

Banking institutions: Profits and stability underpin confidence

In 2024, Tanzania’s banking industry remained profitable, adequately capitalized, and highly liquid, thanks to favorable macroeconomic conditions and prudent fiscal and monetary management. The sector demonstrated resilience to both domestic and external challenges, sustaining upward momentum in deposits, credit growth, and overall asset expansion.

Enhanced regulatory oversight, accommodative monetary policy, and targeted interventions by the BoT – including measures to stimulate private sector lending – played a key role in supporting this growth and maintaining public confidence.

Asset structure: Loans continue to drive expansion

By December 2024, loans, advances, and overdrafts accounted for 58.8 percent of total banking sector assets, highlighting continued credit expansion to businesses and households. Investments in debt securities represented 13.1 percent, while cash holdings and balances with the BoT and other banks stood at 15.4 percent. The remaining 12.7 percent comprised other assets.

Total assets grew by 14.4 percent to TSh 62.2 trillion, up from TSh 54.4 trillion in 2023 – driven largely by higher customer deposits, increased borrowings, and strong profitability. Credit to the private sector also expanded significantly: loans, advances, and overdrafts rose 14.3 percent to TSh 36.6 trillion, compared to TSh 32.0 trillion in 2023. This growth reflects a favorable policy environment and improving business confidence, signaling that banks are increasingly aligning their balance sheets with the country’s real-sector expansion.

Outlook: Building on a stable foundation Looking ahead, Tanzania’s financial sector is expected to maintain its robust trajectory, supported by ongoing investments in digital banking, regulatory reforms to deepen financial inclusion, and continued macroeconomic stability. The challenge for policymakers and institutions alike will be to sustain this growth while expanding access to credit for small and medium-sized enterprises – a key pillar of Tanzania’s development agenda.